Value is dead.

It’s a phrase anyone following the financial press would have heard regularly in recent times. It’s certainly not the first market environment in which value has been killed off by a swathe of commentators and it won’t be last.

It comes as no surprise that value-style investors are existentially challenged during this period of record-breaking market extremes.

This year alone the S&P500 has had 22 record closes during a period in which the index has never been so top-heavy. Year-to-date, five stocks (Facebook, Apple, Amazon, Alphabet and Microsoft) account for around 70% of the move in the S&P500.

At the same time market breadth, the measure of stocks outperforming the index has never been so narrow.Currently just 20 per cent of stocks in the S&P500 are outperforming.

In the chart below you can see US market cap concentration (yellow) and market breadth (dark blue) has now surpassed the previous historical extremes seen during the dot-com bubble.

In light blue, you can see the rolling performance of a global sector-neutral value factor. This provides an insight into how lower multiple stocks have performed on a sector-neutral basis. We currently see this metric also at historical extremes – in negative territory on a three-year rolling return basis.

Even great businesses can de-rate from extremes

Many may argue these nose-bleed valuations of businesses at the top of the market will stand the test of time, because they’re applied to great stocks… New age businesses, disruptors and the leaders of seismic structural change.

This is true… Many are great businesses, however it would be foolish to ignore the fact that as the dot-com bubble burst even great businesses de-rated. Microsoft and Cisco to name just two.

In 1999, Microsoft was trading at a peak multiple of around 85 times earnings. It was then, (and still remains) a great business but 85 times earnings was not the right price to pay. By 2011 the market de-rated this great business to an earnings multiple of less than 10 times. Throughout this period Microsoft’s earnings continued to grow but its share price fell and underperformed the index because the market de-rated the stock.

Those who invested in Microsoft at those nose-bleed multiples, would not have broken even on their investment until 2014.

Following the ‘tech wreck’ and right up to the GFC, there was a major shift in the market narrative in which the lower multiple losers (or value stocks) of the dot-com boom became the new market darlings.

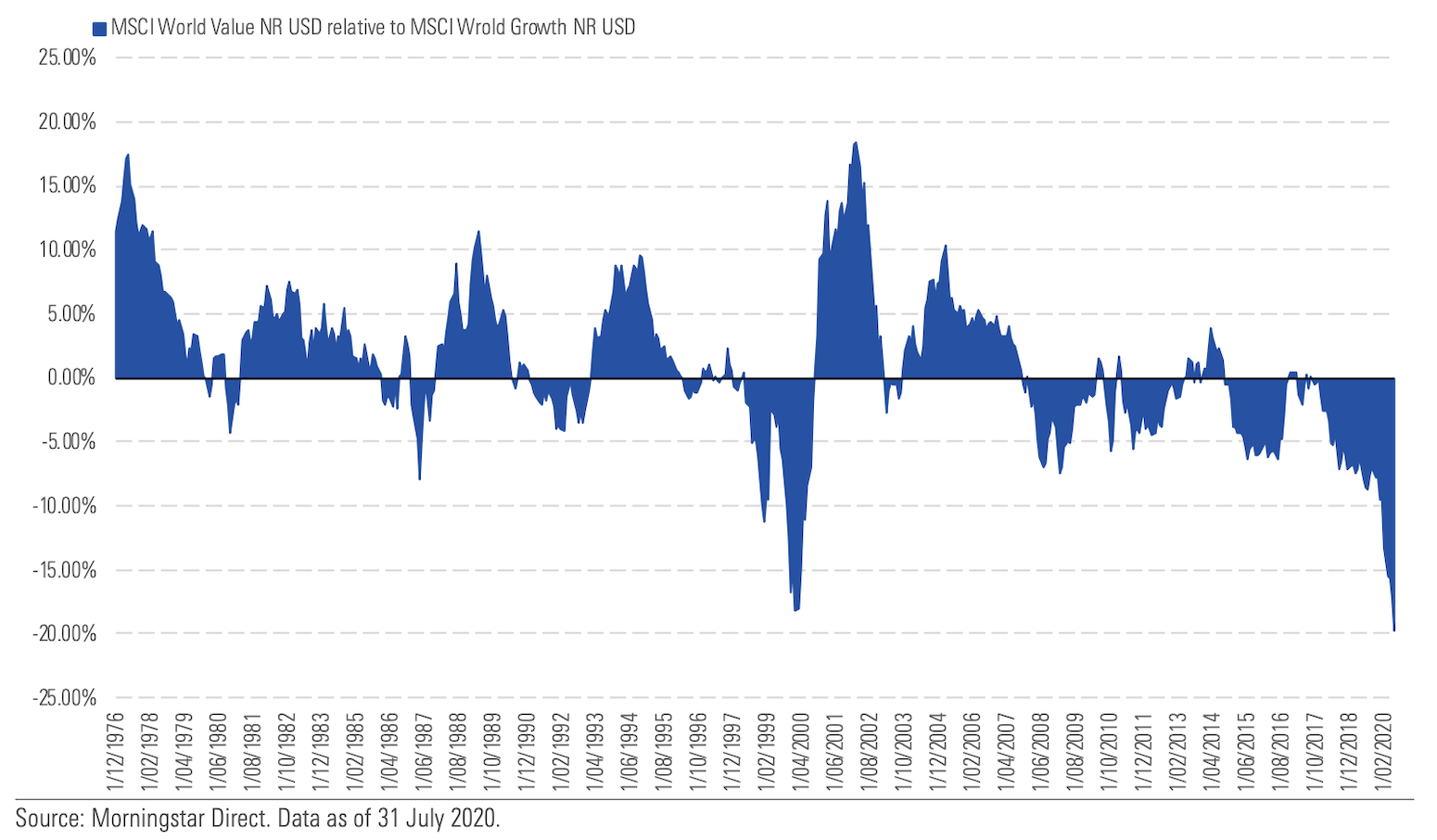

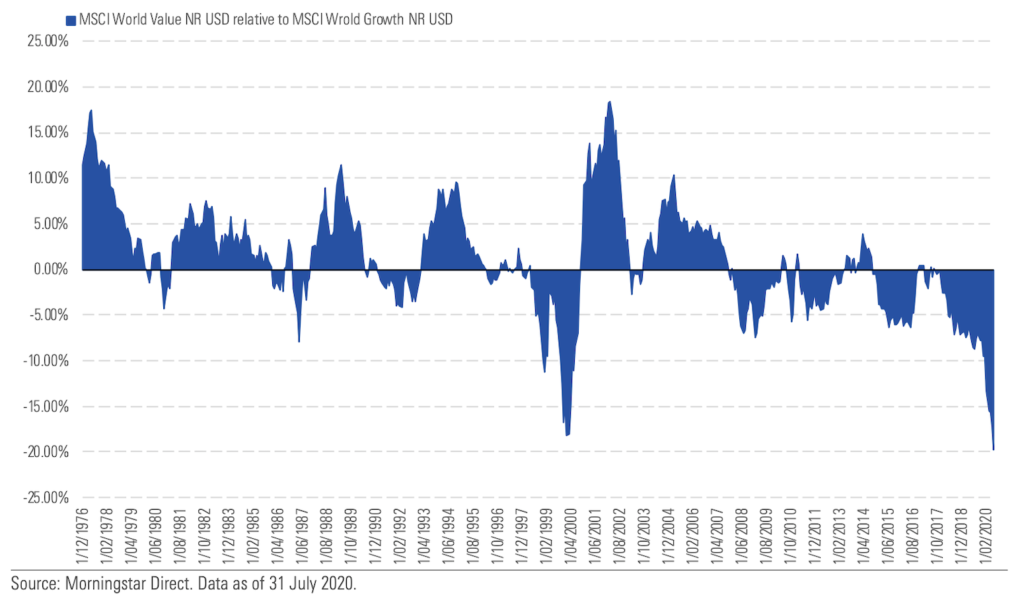

At this point, for anyone still convinced value is dead, it is worth considering the historical performance of value vs growth. The chart below is a striking demonstration. It shows that value-style investing has produced the most consistent returns for investors since the 1970’s, excelling to the highest level of outperformance post the dot-com bubble. What could this outperformance look like given today’s new historical extremes?

Rolling 24-Month Relative Performance of Value vs. Growth

Attempting to place a timeframe on a major cycle shift is futile, but while markets can stay irrational for long periods of time, they can also adjust in the blink of an eye, this is why ignoring value right now is so dangerous.

The recent share market volatility experienced during September was a reminder of the risky game being played by investors who continue to pour capital into growth and momentum.

We know the market extremes outlined above have previously signalled major turning points, where the less popular, lower multiple stocks, begin outperforming the popular market leaders trading on nose-bleed valuations.

Outperformance from these stocks will require a change in today’s narrow narrative as economies cyclically recover from COIVD-19 and stimulus switches from personal income to infrastructure investment. A mild cyclical recovery may be here sooner than many realise as datapoints around a vaccine suggest a positive outcome in the next six months. A vaccine would be material to the lower-multiple parts of the market that benefit from re-opening.

We also see a major tailwind for an emerging cycle shift in decarbonisation, with Asia and Europe leading the charge. Europe’s multi trillion-euro “New Green Deal” announced in 2019 paves the way for a 10 year plus power investment super cycle. Around 12% of our portfolio is exposed to beneficiaries of decarbonisation, many of these are great cyclical business, trading on very low multiples.

Identifying tomorrow’s market winners

Investors shouldn’t buy lower multiple cyclicals simply because they’re cheap. Many are cheap because they are in fact in structural decline.

What we do is simple. We search the world for great businesses, attractively priced with embedded growth opportunities that the market is currently overlooking. A great example right now is Volkswagen Group.

As the focus of the media and the Robinhood investors has been on Tesla, Volkswagen has gone all-in on electric vehicles. Antipodes believes VW may emerge has one of the largest manufactures of EVs. Along with this EV exposure, which is undoubtably a major structural growth opportunity, investors also get exposure to the strong performing luxury brands of Audi and Porsche. This comes at an incredibly cheap multiple, roughly a 30% discount to book and around 6 times our internal future earnings assumptions.

Alibaba is another great business we view as being attractively priced. It may surprise some readers that we’d list an e-commerce giant as a potential winner in a value-orientated market, however Alibaba’s attractive valuation is especially apparent when compared to global peers such as Amazon.

In China, Alibaba is 14 times the size of the largest offline player and hugely dominant across all retail. This is very different to the U.S. market where Amazon’s retail business is only half the size of Walmart. The accelerated adoption of e-commerce in China in the wake of COVID-19 and the opportunity for Alibaba to take share amongst the some 1 billion people that who are becoming increasingly tech savvy in Tier 3 and below Chinese cities are both major tailwinds for growth.

Despite this, Alibaba is currently priced on a CY21 price to earnings ratio of around 20 times. Amazon trades at around 40 times.

These are both examples of what we believe are great business trading at attractive valuations and business we believe have the potential to outperform today’s market leaders in the long term.

Value is more important than ever

There are many investors who today continue to chase growth and momentum. I believe this is an incredibly risky game to play. Blinded by the attraction of short-term gains, they ignore the importance of long term portfolio stability.

We hear much about value traps, and they exist in high numbers in today’s market, but there are likely to be an even greater number growth traps.

Value is alive a well and very attractive opportunities exist for savy investors. In fact, history tells us a value-style exposure in investment portfolios is now more important than ever for anyone wanting a smoother journey to achieving their investment goals.

This article by Jacob Mitchell was originally published by Money Management.

Subscribe to receive the latest insights and updates from Antipodes