When looking for less obvious areas of growth across the globe, we frequently delve into the operations of companies buried within unloved sectors. The automotive sector and its supply chain is one area in which we’re finding an increasing number of value opportunities.

The auto sector frequently graces the headlines for all the wrong reasons – cyclical demand, emissions scandals, the disruptive rise of electric and autonomous vehicles, factory closures and product recalls. It is therefore unsurprising that the sector is extremely cheap relative to both the broader market and its own history.

Look at some of the major players; Honda trades on 7x forward earnings, Volkswagen trades on 6x earnings, Toyota on 9x, GM on 6x and BMW on 8x. Our challenge as investors is to decide whether these low multiples are an accurate reflection of the sector’s prospects or if there are companies within the sector that offer exceptional value.

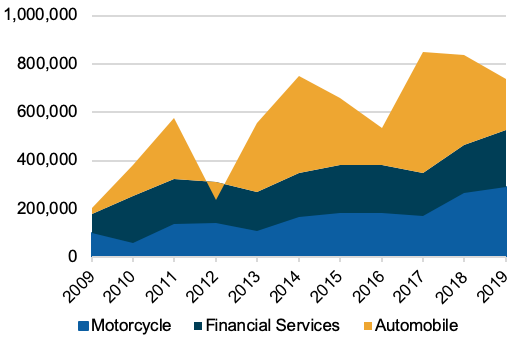

A company we believe provides a compelling investment opportunity is Honda. Honda’s current multiple implies that it is a lower tier automaker with limited prospects. In fact, Honda is a company in robust health with a globally dominant motorcycle franchise, and for whom making cars is only its third most lucrative business. The growing earnings from the Motorcycle and Financial Services businesses have acted as an offset to the volatility of the Automotive profit stream.

Honda operating profit by division (JPY, Bn). Source: Factset.

Irrational extrapolation

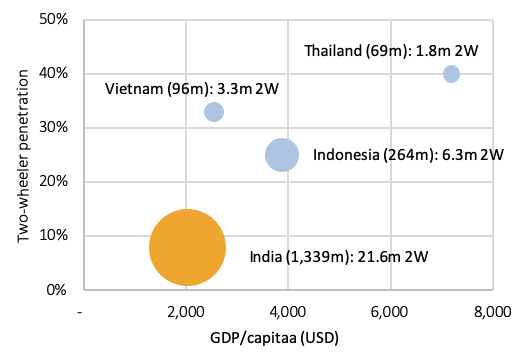

The best asset within Honda is its motorcycle business, with 2-wheelers increasingly the mobility choice of consumers in emerging markets. In the post–crisis period Honda’s Motorcycle business has grown revenues at a compound rate of 7% and now controls around 25% of the global motorcycle market. The biggest opportunity for the motorcycle business is India.

Our proprietary research of the global motorcycle market shows a positive correlation between the size of an emerging nation’s 2-wheeler market and all of GDP per capita, urbanisation rate and population age. Forecasts of all these variables point to higher rates of Indian motorcycle ownership in the coming years. In fact, we believe that the Indian motorcycle market, which is already the largest in the world, has the potential to roughly double in unit terms over the coming decade driven by a growing, aging and increasingly affluent population. The example of other emerging markets is supportive of that thesis.

Figure 3: Two-wheeler volume and penetration relative to GDP/capita (USD) and population. Source: Antipodes, Factset

In addition to the growth in the overall Indian market we expect Honda to further increase its share, which has already nearly doubled from 14% in 2010 to 27% in 2018. Honda has become dominant in some of the world’s most important motorcycle markets (Vietnam, Indonesia and Thailand) with between 70–82% share. Learnings from these markets will be supportive of gradual share gain in India facilitated by Honda’s control of the supply chain for key emissions control components, which we discuss further below.

Honda’s global motorcycle business has posted 6 consecutive years of double-digit operating margins, making it comfortably Honda’s most profitable manufacturing business. A counterweight to that strong performance has been the underwhelming performance of the Automotive business. Honda’s issues in the automotive business are margin related as opposed to technology, demand or brand equity – all of which they have in abundance. Honda today is delivering operating margins in the low single digit range, global peers achieve margins in the mid to high single digit range.

The Automotive margin has been sliding since 2002 due to poor execution. The business has had the wrong products, with too many small cars and sedans and not enough SUVs, and a growth obsession within a multi-regional structure. This has led to much of the growth being unfocused, with too much capacity producing too many models with too many variants. The prior “Vision 2020” strategy sought 6 global regions which were largely self-reliant, increasing complexity and significantly impairing the synergies that the company’s scale could deliver.

The goal of the new Automotive strategy is to heal these self-inflicted wounds and improve profitability through three main actions – lowering costs whilst increasing capacity utilization and increasing the commonality of production by moving to a new platform.

It’s also worth mentioning Honda’s evolving partnership with GM, which has some interesting facets. Honda will invest just under $3 billion over the next 12 years in GM’s Cruise, allowing access to GM’s autonomous technology. They have a joint fuel cell manufacturing plant and are working together on “next generation” batteries. This is a sensible industrial tie up, defraying the cost of development over more vehicles than each would have alone.

The third pillar of Honda’s business, and the second most important in earnings terms after the Motorcycle business, is the financial services company which facilitates customers to buy vehicles, largely in the US. It’s a compelling business which has an option of first refusal to extend finance to the customers they wish to adopt given the proximity at the point of sale. The scaled dealership network offers Honda lower costs of servicing than third party finance providers. That charge offs peaked at just 55 basis points during the Global Financial Crisis is testament to the underwriting quality of the customer base that Honda’s financial services business accepts.

Multiple ways of winning

Competitive dynamics & product cycle

Honda has a strong brand in the automotive sector, and the internally focused restructuring will be aided by a major model cycle with roughly 50% of the line-up refreshing over the coming two years or so, including the hugely important Civic and CR-V, with that new volume coming against a restructured cost base.

New model launches will also increasingly be on the company’s new automotive platform, known as Honda Architecture. This follows the well-trodden path of many global automakers in increasing the commonality of processes and parts used on different models to bring procurement scale, manufacturing flexibility and efficiency. The full benefit of this new platform will not be felt until 2027 but begins with the high volume Civic next year.

Regulatory

The Indian Government is progressively rolling out new vehicle emission standards. From April 2020, all new motorcycles sold in India will be required to have BS6 emissions standard compliant engines. This should allow Honda to take market share because subsidiary supplier, Keihin, controls 70–80% of the market for fuel injection systems – the key item for BS6 compliance. In addition, anti-lock braking systems are becoming mandatory on all bikes with engines over 125cc. This will provide another competitive advantage as Honda subsidiary, Nissin Kogyo, a brake manufacturer, controls 60–70% of the Indian market.

This captive supply chain represents a major competitive advantage. The company has indicated it will use any related manufacturing cost advantage to add features to bikes, such as LED lights or a smart key, in order to make models more attractive rather than just offer a lower price.

Honda ranks second with 27% share in the Indian market behind Hero but, post the introduction of the BS6 standards, aims to get to first with around 30% share. It should be mentioned that in the near-term the Indian automotive market is going through a rocky patch with weaker economic growth, limited credit availability and volatility around emissions standards. These factors, however, don’t alter the fundamentally strong long-term adoption opportunity.

Management and Financial

Honda has a fortress balance sheet and is in excellent financial health. The structural growth in the motorcycle business and targeted margin improvement in the automotive business should yield materially higher earnings over time, for which we are paying a low multiple today.

Honda has undergone significant management change in the past four years, with all the top roles transitioning in that period and culminating with the change of Chairman in April of this year. The Motorcycle business has performed exceptionally well during that period, whilst the process of rectifying the underperforming Automotive business has been slower than we would have hoped. The new plan, which was only communicated this year, is the right solution to the challenges of the business. We expect increased front-footedness from management in the coming quarters, along with improving financial delivery.

Style and Macro

Throughout the current protracted period of low rates and concerns over global growth, investors have been paying increasingly high multiples for businesses with defensive and structural growth qualities. Honda represents an attractive way for investors to gain such style exposure, that is, adding a cheaper expression of quality growth to portfolios.

Margin of Safety

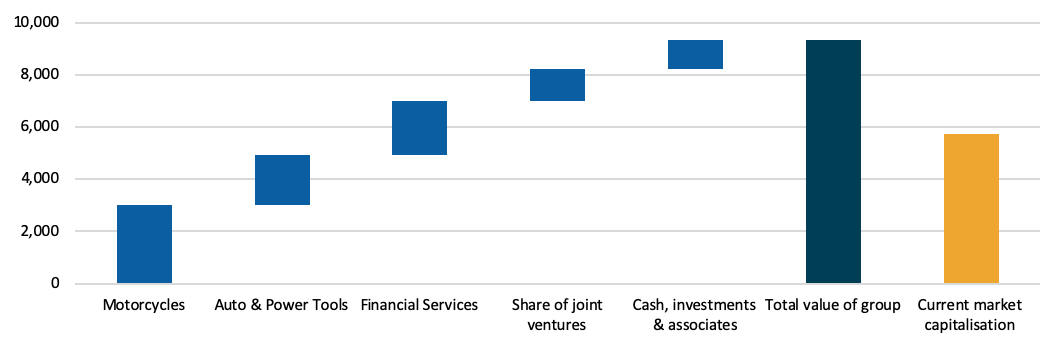

Honda’s valuation is incredibly attractive with ¥2.57 trillion of cash on the balance sheet against a market cap of ¥4.5 trillion. The industrial business alone, excluding the Honda Finance Company, has nearly ¥2 trillion of cash. It trades on an ex-cash 2021 PE of a little over 2x. A sum of the parts implies the shares are materially undervalued.

In fact, the hardest question to answer when considering an investment in Honda Motor is “which bit do you want for free?” As we demonstrate in the following chart, at the current market valuation you would be getting at least one of the major divisions of the business, all of which we consider attractive, for nothing.

Honda value by division (JPY, B). Source: Factset

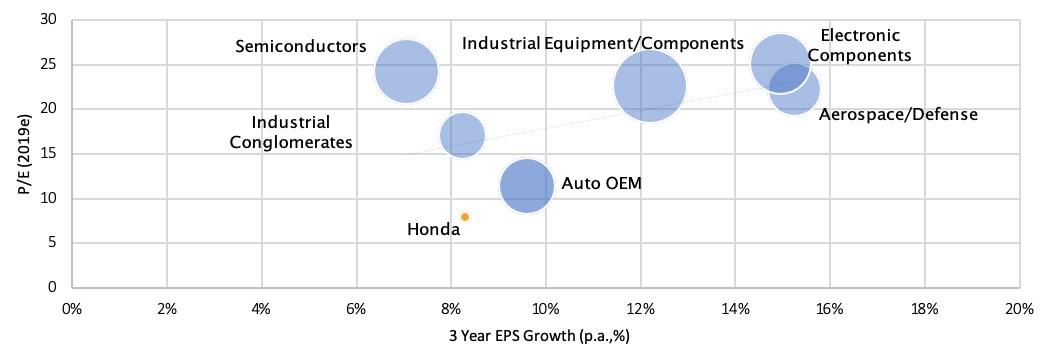

Honda valuation multiples v peer groups. Source: Antipodes, Factset