The article was first published in Citywire Wealth Manager 10 May 2022.

Antipodes Partners’ Jacob Mitchell is uncovering long-term secular trends at attractive valuations.

Following two years of uncertainty in markets, dominated by the Covid-19 pandemic, 2022 promised to be a year marked by a return to relative stability. Instead, global geopolitical events, heightened volatility and accelerating inflation have created another challenging landscape for global investors.

While a degree of caution is clearly necessary in the current context, the uncertainty has created opportunities to gain exposure to long-term secular trends at attractive valuations.

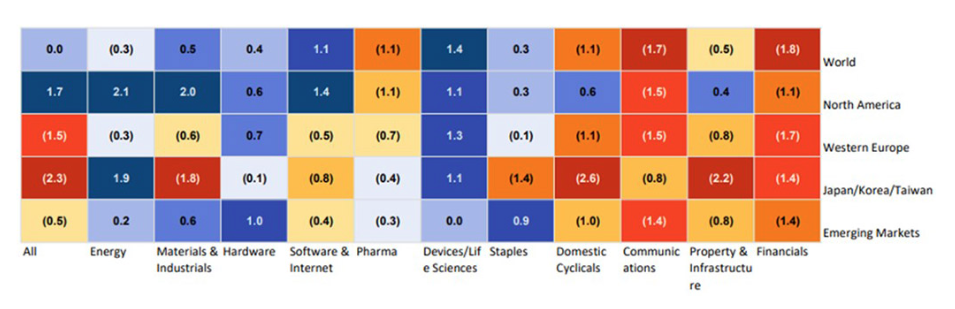

Our valuation heatmap, shown below, provides a granular illustration of the clusters of value we see in the current market.

It is based on the degree to which a sector’s enterprise value to sales multiple, relative to the world, is above or below its 22-year trend, expressed in terms of the number of standard deviations from the mean.

The warmer the colour, the greater the relative multiple to history – and vice versa for the cooler blues. Within the more value-oriented areas, we see several particularly appealing investment opportunities.

Stagflation requires focus on quality

The start of February saw a consensus-beating inflation print of 7.5% in the US, with constituent increases looking very broad based, pointing to ongoing pressures as the year continues.

In previous market and economic drawdowns, the Fed has responded by pivoting policy and injecting liquidity, but the inflationary environment is a real barrier to this at the present time. The situation is similar in the EU, where the ECB faces the challenge of inflationary pressures while ensuring economic stability through the conflict.

This backdrop points to a period of stagflation, which would be challenging for weak cyclicals and weak or expensive growth stocks. Instead, we are focusing on resilient businesses, such as Oracle and SAP in the enterprise software space.

These businesses have strong pricing power, reliable demand, and are inflation protected, but are valued at a discount to peers at 16x and 20x earnings, respectively.

Decarbonisation trend to accelerate

Russia’s invasion of Ukraine has led to substantial shifts in commodity prices, with widespread sanctions on Russian oil and gas pushing oil prices to highs not seen in more than a decade. Energy independence has been pushed rapidly up the news agenda by the conflict, and this will have significant implications for the entire energy sector.

In recent years, Europe has relied on Russia for 40% of its natural gas supplies and 20% of oil supplies, and these supplies cannot easily be made up elsewhere. As a result, the continent’s broad transition away from fossil fuels is only likely to accelerate.

One company that is potentially well-placed to both contribute to and benefit from this shift is Siemens Energy. The business provides energy efficient grid systems, gas and wind turbines and is valued at just 8x Ebita. At the same time, we have also added to our holdings of US oil and gas companies, which should see a boost over the short and medium term as demand for Russian oil is diverted elsewhere.

Opportunities in industrial innovators

While markets have understandably been fixated on short-term drivers, we are also looking at the bigger picture, with broader trends towards more efficient buildings and electric vehicles set to continue for years to come. These trends create opportunities for some innovative industrial businesses, which can be found at appealing valuations due to short-term macro factors.

One such business is Norsk Hydro, one of the largest aluminium producers in the world. Despite impressive share price growth over the past year, we believe the market is yet to fully appreciate the wider supply and demand dynamics for aluminium and Norsk Hydro’s unique position in the market.

Aluminium is lighter than steel and stronger for its weight, yet also more recyclable. Demand for the metal predominantly comes from the construction and transport sectors, where reducing emissions is an increasingly significant driver of decision-making.

In this context, what sets Norsk Hydro apart is it produces its aluminium using hydroelectricity, instead of the traditional coal. Its carbon emissions per tonne of aluminium are around a quarter of the average producer, and the company continues to invest in R&D with a view to producing carbon-free aluminium in the future.

Despite being ideally positioned to benefit from the unstoppable trend towards decarbonisation, the stock is currently valued at 16x earnings. This is a reasonable discount to the replacement cost of its unique assets, making it a compelling option for investors looking for innovative industrial businesses for the long-term.

Subscribe to receive the latest news and insights from the Antipodes team

This communication was prepared by Antipodes Partners Limited (ABN 29 602 042 035, AFSL 481 580) (Antipodes). Antipodes believes the information contained in this communication is based on reliable information, no warranty is given as to its accuracy and persons relying on this information do so at their own risk. This communication is for general information only and was prepared for multiple distribution and does not take account of the specific investment objectives of individual recipients and it may not be appropriate in all circumstances. Persons relying on this information should do so in light of their specific investment objectives and financial situations. Any person considering action on the basis of this communication must seek individual advice relevant to their particular circumstances and investment objectives. Subject to any liability which cannot be excluded under the relevant laws, Antipodes disclaim all liability to any person relying on the information contained on this website in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information.

Any opinions or forecasts reflect the judgment and assumptions of Antipodes on the basis of information at the date of publication and may later change without notice. Any projections are estimates only and may not be realised in the future. Information on this website is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained on the website is prohibited without obtaining prior written permission from Antipodes.

Pinnacle Fund Services Limited ABN 29 082 494 362 AFSL 238371 is the product issuer of funds managed by Antipodes. Any potential investor should consider the relevant Product Disclosure Statement available at www.antipodesonespartners.com when deciding whether to acquire, or continue to hold units in a fund. The issuer is not licensed to provide financial product advice. Please consult your financial adviser before making a decision. Past performance is not a reliable indicator of future performance.